Page Contents

- What Is Capital Gain Tax on Property In India?

- Short-Term Capital Gain Tax On Property

- How To Save Short-Term Capital Gain Tax?

- Calculation of the Short-Term Capital Gain Tax

- Example For The Calculation of Short-Term Capital Gain Tax

- Long-Term Capital Gain Tax on Property

- How To Save Long-Term Capital Gain Tax on Property?

- Calculation of the Long-Term Capital Gain Tax

- Example For The Calculation of Long-Term Capital Gain Tax

- Difference Between Short-Term Capital Gain Tax and Long-Term Capital Gain Tax

- Capital Gains Deposit Account Scheme

- Opening The Capital Gains Deposit Account

- Conditions for Saving The Capital Gain Tax

- Capital Gain Tax on the Inherited Properties In India

- FAQs

What Is Capital Gain Tax on Property In India?

The profit that you get by selling the property is considered income. Therefore, you need to pay the tax on the profit or gain from selling the property. This Tax on the Capital Assets is termed Capital Gain Tax.

Real estate properties come under the category of capital assets. Hence, after selling the properties, you need to pay the Capital Gains Tax. Capital Gains Tax is categorized as Short-Term Capital Gain Tax and Long-Term Capital Gain Tax.

It is mandatory to pay the Capital Gain Tax on the property as per section 45 of the Income Tax Act.

Short-Term Capital Gain Tax On Property

The profit or gain from selling the property with a holding period below 2 years is a short-term capital gain. The tax applied to this gain is called Short-Term Capital Gain Tax.

The holding period for the Short Term Capital Gain for the various assets is as follows:

| Asset | Holding Period |

|---|---|

| Immovable Properties (Land, House, Building) | Less Than 2 Years |

| Listed Shares In Stock Exchange, Mutual Funds, Debentures, Government Securities, Units of UTI, Zero-Coupon Bonds | The holding period for STCG on Listed Equity and Equity-Oriented Mutual Funds is 12 months. For Debt Mutual Funds purchased after April 1, 2023, all gains are taxed as STCG regardless of the holding period. |

| Other Capital Assets, Unlisted Debentures, Units of Debt Fund, Other Immovable Properties | Other capital assets are generally short-term if held for 2 years or less, subject to specific rules for certain assets such as debt mutual funds. |

“From the Budget 2024 / post-23 July 2024 framework, the criteria have been updated for the immovable property, such as plot, house, commercial spaces, etc. Currently, the Short Term Capital Gain tax is considered a gain from holding the property for less than 2 years (24 months).”

Please note that Section 111A specifically applies to short-term capital gains on listed equity shares, equity-oriented mutual funds, and units of business trusts. Short-term gains on immovable property are governed by the general provisions of the Income Tax Act and added to your total taxable income.

To calculate the applicable taxes, the short-term capital gain is classified as:

- Short-term capital gains that are covered under section 111A.

- Short-term capital gains other than those covered under section 111A.

| Short-term capital gains covered under section 111A. | Short-term capital gains other than those covered under section 111A. | |

|---|---|---|

| Applicable On | Listed equity shares, equity-oriented mutual funds, and units of business trusts; short-term gains on these transfers are taxed at 20% for transfers on or after 23 July 2024. | Immovable Property such as Land, House, or Building. Items like Gold and Silver, Bonds, and Government Security. |

| Applicable Tax | As per the Budget 2024 revisions, the tax rate for short-term capital gains under Section 111A has been increased to 20% from the previous 15%. | Tax is Applicable as per the Annual Income Slab. |

| Tax Savings | Sections 80C to 80U reduce total taxable income, but they do not provide a separate exemption for short-term capital gains on property. | Sections 80C to 80U reduce total taxable income, but they do not provide a separate exemption for short-term capital gains on property. |

So, here we can conclude that the applicable tax for immovable properties, such as land, house, or building tax, is applicable as per the annual income slab since it does not come under section 111A.

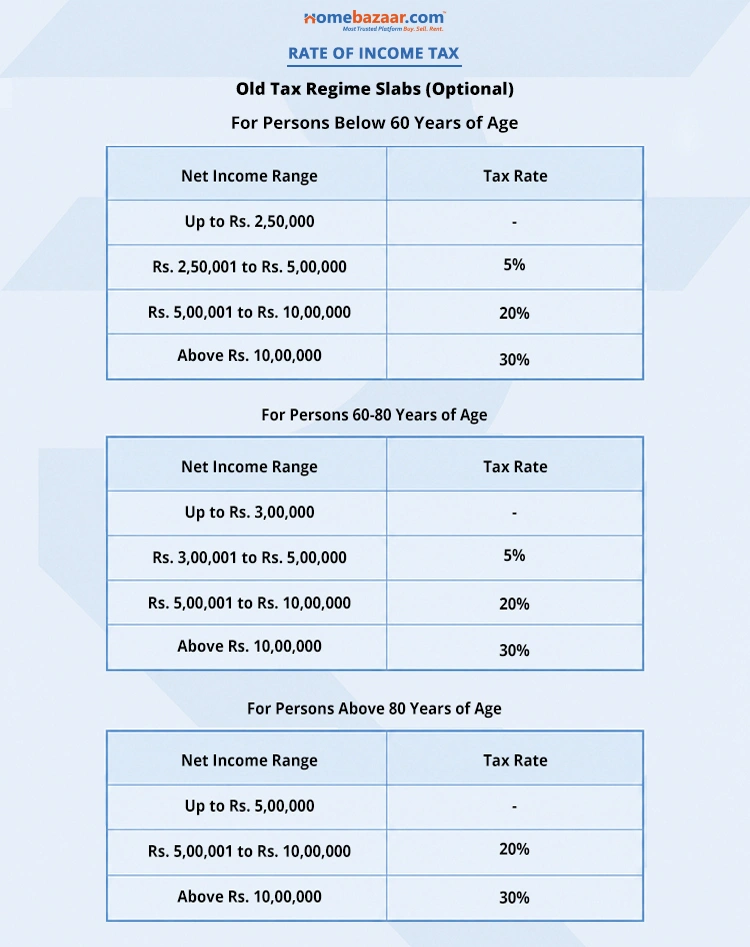

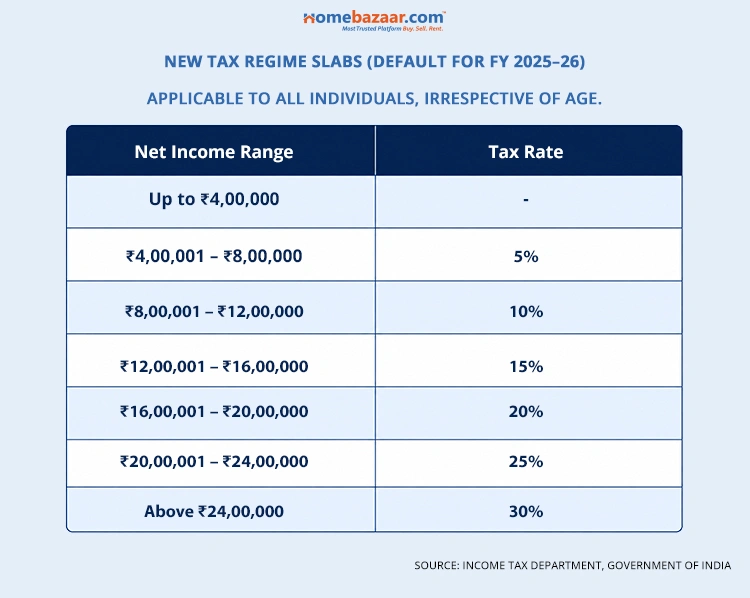

Since the gain or profit from selling the property is considered income, the tax for the Short Term Capital Gain from the real estate properties is calculated on the basis of the Annual Income Tax Slab.

Here Are The Annual Income Tax Slabs –

How To Save Short-Term Capital Gain Tax?

The taxes on the short-term gains on the real estate properties can be deducted under sections 80C and 80U. However, deductions under Sections 80C and 80U can reduce your total taxable income, but they do not specifically exempt short-term capital gains from property.

As per section 80C, you can get the Tax Concession up to Rs 1.5 Lakh.

The 80U is for persons with disabilities, and the concession is up to Rs. 75,000/- for Normal Disability and Rs. 1,25,000 for Severe Disability.

Section 80C is a deduction for investments like PPF or LIC and is capped at ₹1.5 lakh. It is not a reinvestment exemption for capital gains like Section 54, and it does not allow you to “wipe out” large gains from property sales.

You can reduce the Capital Gain Tax by following investment options under section 80C:

- Public Provident Fund

- National Pension Scheme

- Fix Deposit Investment for 5 Years

- Unit Linked Insurance Plan (ULIP)

You can save the Capital Gain Tax by making payments in the following options under section 80C:

- Life Insurance Premium

- Home Loan Repayment

- Stamp Duty and Registration

- Provident Fund

- Deductions Under EPF

Calculation of the Short-Term Capital Gain Tax

The formula for calculating the Short Term Capital Gain Tax is as follows:

Where –

Where –

- Sales Consideration is the selling price of the property

- The expenditure incurred while selling the property, which involves-

- The brokerage

- Advertisement expenses

- Stamp Paper and Documentation Cost

- The Cost of Acquisition is the buying cost of the property

- The Cost of Improvement is the capital expenses incurred to enhance the asset, such as renovation, structural changes, etc.

Example For The Calculation of Short-Term Capital Gain Tax

Consider that you purchased a property worth Rs. 80,00,000 in April 2025 and sold it in April 2026 for Rs. 90,00,000. The holding period, in this case, is 1 year. You paid the brokerage of Rs 50,000 for selling the property. And your annual income is Rs 5,00,000.

In this case-

- The property is held for less than 2 years, and hence it will be marked as Short Term Capital Gain.

- Since the short-term capital gain is obtained from the immovable property, it does not come under taxation under Section 111A.

- Therefore, in this case, the tax will be applicable as per the income tax slab set by the Income Tax Department.

The Total Short Term Capital Gain =

[Sales Consideration of Asset – Cost of Acquisition- Expenditure incurred for the transfer of property]

= [90,00,000 – 80,00,000 – 50,000]

Short Term Capital Gain = Rs. 9,50,000.

Adding short-term capital gain to annual income = ₹9,50,000 + ₹5,00,000 = ₹14,50,000.

From the Income Tax Slabs, income above ₹10 lakh falls into the 30% slab, but tax is calculated progressively across all applicable slabs.

STCG on property is added to your total income and taxed according to Income Tax Slabs. This means the tax is calculated progressively (e.g., 0% on the first threshold, 5% on the next, and so on) rather than applying the highest slab rate to the entire amount.

Short Term Capital Gain Tax = Under the old tax regime for FY 2026–27, tax on ₹14,50,000 would be approximately ₹2,47,500 before cess, calculated progressively across slabs (calculated as: Nil on 2.5L + 12,500 on next 2.5L + 1,00,000 on next 5L + 1,35,000 on the remaining 4.5L at 30%).

You can claim deductions under Sections 80C and 80U while computing your total taxable income.

Long-Term Capital Gain Tax on Property

The profit or gain from selling the property with a holding period of more than 2 years is a long-term capital gain. The tax applied to this gain is called Long Term Capital Gain Tax.

The holding period for the Long Term Capital Gain for the various assets is as follows-

| Asset | Holding Period |

|---|---|

| Immovable Properties (Land, House, Building), Other Capital Assets, Unlisted Debentures, Other Immovable Properties | More Than 2 Years |

| Listed Shares In Stock Exchange, Mutual Funds, Debentures, Government Securities, Units of UTI, Units of Debt Fund, Zero-Coupon Bonds | Holding periods differ by asset class; for immovable property, the long-term threshold is more than 24 months, while listed equity shares and equity-oriented mutual funds generally have a 12-month threshold. |

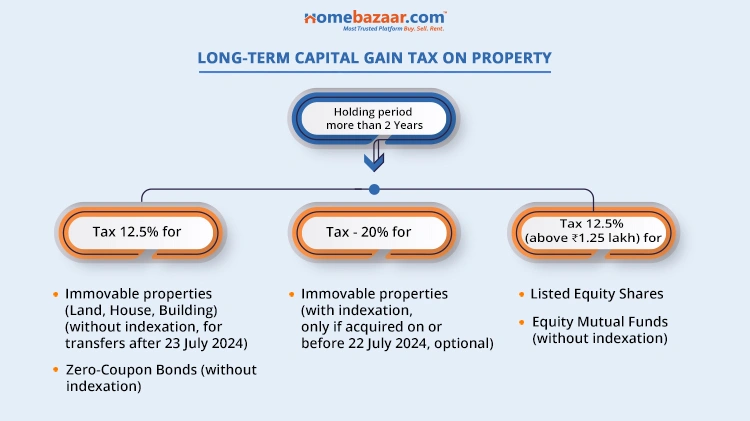

Since 2024, the criteria have been updated for the immovable property. Currently, the Long Term Capital Gain is considered a gain from holding the property for more than 2 years (24 months).

For property transferred on or after 23 July 2024, LTCG is taxed at 12.5% without indexation, while eligible properties acquired on or before 22 July 2024 may still use the 20% with indexation option if it is more beneficial.

Long-term capital gains on listed equity and equity-oriented mutual funds are taxed at 12.5% for gains exceeding ₹1.25 lakh in a financial year.

How To Save Long-Term Capital Gain Tax on Property?

Section 54 gives the relaxation on selling the residential property and acquiring the new residential property. Following is the complete list of section 54 and the subsections to get the concessions by reinvesting profits or gains in new assets as per section 54.

| Section | Conditions For Exemption |

|---|---|

| Section 54 | Capital Gain on residential properties is spent on buying a new residential property. Exemptions under Section 54 for reinvestment in a residential house are capped at a maximum of ₹10 Crore. |

| Section 54 B | Section 54B applies when capital gains from the sale of agricultural land are reinvested in purchasing new agricultural land. |

| Section 54 D | Section 54D applies when land or building used by an industrial undertaking is compulsorily acquired, and the gains are reinvested in land or building for shifting, re-establishing, or setting up the undertaking. |

| Section 54EC | Section 54EC provides an exemption when capital gains are invested in specified bonds such as NHAI or REC. |

| Section 54EE | The Capital Gain is reinvested in long-term specified assets. |

| Section 54F | The Capital Gain is reinvested in buying residential properties. Exemptions under Section 54F for reinvestment in a residential house are capped at a maximum of ₹10 Crore. |

| Section 54G 54GA | On the transfer of assets in cases of the shifting of an industrial undertaking from an urban area. |

Calculation of the Long-Term Capital Gain Tax

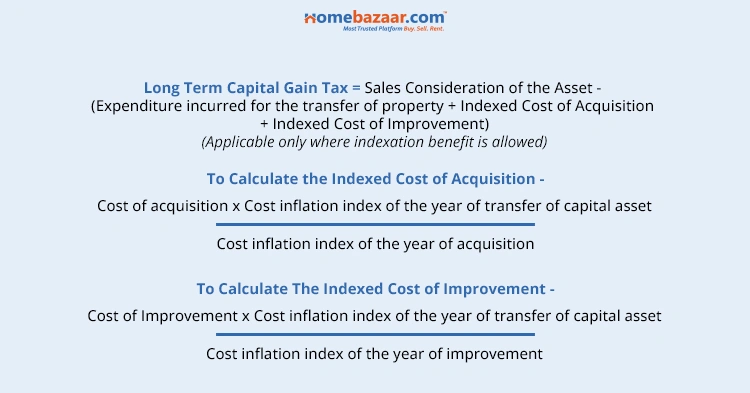

The long-term capital gain tax can be calculated by using the following formula.

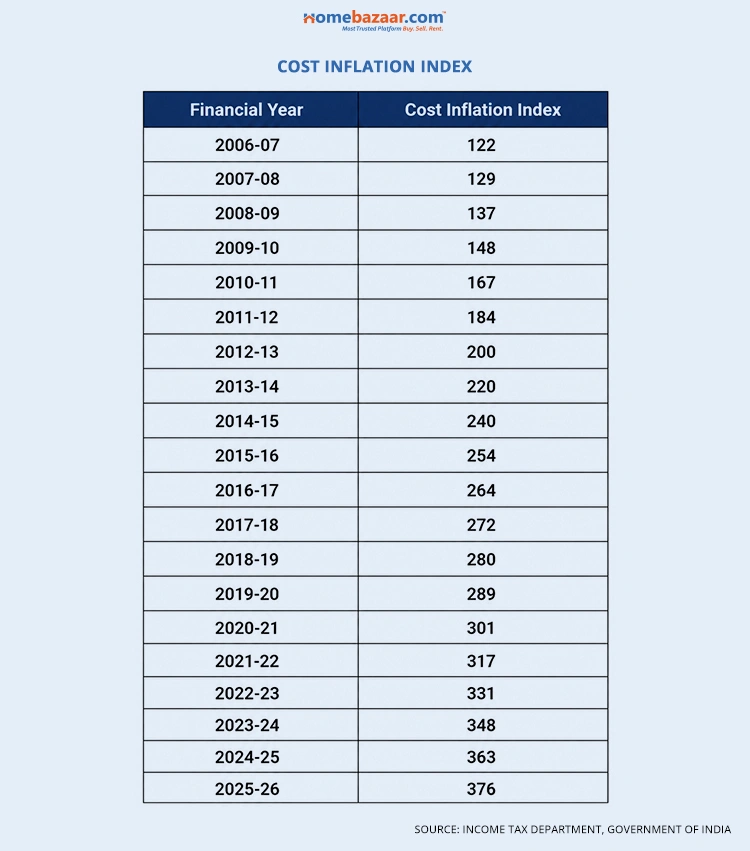

The cost inflation index of the particular year is important for the calculation of the long-term capital gain tax.

The cost inflation index is set by the Central Government. The list of the inflation index is as follows-

Example For The Calculation of Long-Term Capital Gain Tax

Consider that you purchased a residential property in the year 2010 at Rs 50,00,000 and sold it in the year 2020 for Rs 1,20,00,000. You paid the brokerage of Rs 20,000.

In this case-

- The property has been held for more than 2 years, and hence it will be considered as Long Term Capital Gain.

- Because this property was sold in 2025, the current LTCG rule applies. For property transferred on or after 23 July 2024, LTCG is generally taxed at 12.5% without indexation, though eligible resident individuals and HUFs may opt for 20% with indexation if it is more beneficial.

Sales Consideration of the property = Rs 1,20,00,000

Cost of acquisition (Purchase Price) = Rs 50,00,000

Expenditure incurred for the transfer of property (Brokerage) = Rs 20,000

Cost Inflation Index of the year 2015–16 = 254.

The Cost Inflation Index for FY 2025–26 = 376.

To Calculate the Indexed Cost of Acquisition-

Cost of acquisition × Cost Inflation Index of the year of transfer / Cost Inflation Index of the year of acquisition

[50,00,000 × 376] / [254] = Rs 74,01,574.80

Long Term Capital Gain = Sales Consideration – (Expenditure on transfer + Indexed Cost of Acquisition + Indexed Cost of Improvement)

= 1,20,00,000 – [20,000 + 74,01,574.80 + Not Applicable]

Long Term Capital Gain = Rs 45,78,425.20

Now the Long Term Capital Gain Tax = 20% of Rs 45,78,425.20

Long Term Capital Gain Tax = Rs 9,15,685.04

“The Long Term Capital Gain gets the benefit of indexation under the eligible 20% regime. For property transferred on or after 23 July 2024, indexation is not available under the new 12.5% regime, but resident individuals and HUFs may opt for 20% with indexation for land or building acquired before 23 July 2024 if that is more beneficial.”

Difference Between Short-Term Capital Gain Tax and Long-Term Capital Gain Tax

| Short-Term Capital Gain Tax | Long-Term Capital Gain Tax |

|---|---|

| Applicable to the Profit or Capital Gain from holding the property for less than 2 years. | Applicable to the Profit or Capital Gain from holding the property for more than 2 years. |

| For immovable properties such as land, building, or house, the tax applied is applicable as per the income tax slabs. | Under the older indexed method, LTCG is taxed at 20% plus surcharge and cess; under the post-23 July 2024 rule, the tax rate is 12.5% without indexation for applicable transfers. |

| Short-term capital gains (STCG) on property are added to your total income and taxed at your applicable slab rates; while Section 80C deductions can reduce your total taxable income, they cannot be specifically used to offset capital gains. | The relevant exemptions include Sections 54, 54B, 54D, 54EC, 54EE, 54F, 54G, and 54GA. |

| The Tax Exemption can be up to 1.5 Lakh under 80C. Where the 80U is applicable for Normal Disability: Rs. 75,000/- Severe Disability: Rs. 1,25,000/- | Section 54 exemption is capped at ₹10 crore, and a one-time option to invest in two residential houses is available only where the capital gain does not exceed ₹2 crore. |

Capital Gains Deposit Account Scheme

To get the benefit of the tax deductions on the Capital Gains, you need to reinvest the amount within the given time period. The Capital Gains Deposit System, introduced in 1988, allows you to park the Capital Gains till you find suitable reinvestments as per Section 54.

The Capital Gains Deposit System benefits you in the following ways –

- Safeguards the Capital Gains before investing in the appropriate options as per the tax exemption criteria

- Ensures that you don’t miss the applicable tax exemptions

- Get sufficient time to acquire new assets from the Capital Gains

- Get the interest as per the Savings Bank / Fixed Deposit rates

Opening The Capital Gains Deposit Account

You can open the Capital Gains Deposit Account in any authorized bank. There are two different types of Capital Gains Deposit options – Type A and Type B. Type A Capital Gains Deposit Accounts are similar to a savings account. It has a simple interest that is paid at regular intervals. Type B is similar to fixed deposits and has a maximum 3-year term.

Any amount withdrawn from a CGAS account must be used for the specified investment within 60 days, and any unutilised amount should be redeposited. The first withdrawal is made using Form C, and subsequent withdrawals are made using Form D.

Conditions for Saving The Capital Gain Tax

- To claim exemption under Section 54, you must purchase a new residential house within 1 year before or 2 years after the sale, or construct one within 3 years. The 6-month limit applies specifically to Section 54EC (investing in specified bonds like NHAI/REC).

- For Section 54 and Section 54F, the new house is generally subject to a 3-year lock-in, while Section 54EC bonds have a 5-year lock-in.

- If the amount invested in the new asset is lower than the capital gain, exemption is allowed only to the extent of the amount invested.

- If you reinvest only part of the capital gain, the tax exemptions are applicable only on the reinvested amount.

- To get the exemptions under 54, the new residential property should be purchased 1 year before or 2 Years after the sale of the existing property on which Capital Gain was received.

- Under Section 54, if the capital gain is more than the cost of the new property, only the invested portion is exempt, and the remaining balance is taxable. The gain does not have to be less than the property value for the exemption to apply.

Basic Exemption Limits for Total Income

| Age | Exemptions Limit |

|---|---|

| Below 60 Years | Rs. 2,50,000 |

| 60-80 Years | Rs. 3,00,000 |

| Above 80 Years | Rs. 5,00,000 |

These figures refer to the Basic Exemption Limit for total annual income, not a specific limit for capital gains tax. Under the New Tax Regime (default for 2025), the basic exemption limit is a uniform ₹3,00,000 for all individuals regardless of age, though residents can still use their unused basic exemption to offset LTCG.

Capital Gain Tax on the Inherited Properties In India

If the property is received by inheritance or gift, the Capital Gain Tax is not applicable to it. However, if you sell the property received by inheritance or gift, then the tax is applicable on the capital gain.

Here are the conditions for the calculation of the Capital Gain Tax on Inherited Properties:

- The cost of acquisitions will be the cost to the previous owner of the property

- For inherited property, the indexation benefit is generally calculated from the year the previous owner originally acquired the asset.

- The formula for the calculation of the Capital Gain Tax remains the same.

FAQs

- What is Short-Term Capital Gain Tax on Property?

The profit or gain from holding the property for less than 2 years is called the short-term capital gain. The tax applicable to the short-term capital gain is called the Short-Term Capital Gain Tax. - What is Long-Term Capital Gain Tax on Property?

The profit or gain from holding the property for more than 2 years is called the long-term capital gain. The tax applicable to the long-term capital gain is called the Long-Term Capital Gain Tax. - How to Calculate the Short-Term Capital Gain Tax?

The Short-Term Capital Gain Tax can be calculated by using the following formula:

Short Term Capital Gain Tax = Sales Consideration of Asset – Expenditure incurred for the transfer of property- Cost of Acquisition. - How to Calculate the Long-Term Capital Gain Tax?

The Long-Term Capital Gain Tax can be calculated by using the following formula:

Long Term Capital Gain Tax = Sales Consideration of the Asset – [Expenditure incurred for the transfer of property + Indexed Cost of Acquisition + Indexed Cost of improvement] - How to save the Short-Term Capital Gain Tax?

Short-term capital gains from property are treated as normal income and taxed as per your slab rate. While Section 80C and 80U deductions can reduce your total taxable income, they cannot be specifically claimed against capital gains to lower that specific tax component directly. The maximum amount for the exemption can be up to Rs 1.5 lakh. - How to save the Long-Term Capital Gain Tax?

Exemption under Section 54 is based on the actual amount reinvested in a new property, capped at ₹10 crore, and is not determined by the taxpayer’s age category. - What is the Capital Gains Deposit Account Scheme?

The capital gains deposit account scheme allows you to park your Capital Gains till you find the right reinvestment options. This ensures that you don’t miss the applicable tax exemptions. - What is the Capital Gain Tax on the inherited properties in India?

There is no capital gain tax applicable to inherited or gifted properties. However, the capital gain tax is applicable on the profit from the sale of Inherited or gifted properties.